President Trump Signs The GENIUS Act

Newsletter Issue 63 (Law Reform): A new legal framework now governs stablecoins in the US

President Donald J. Trump has just signed a new law that creates federal rules for stablecoins used as a form of payment. Known as the GENIUS Act, this legislation sets legal requirements for who can issue stablecoins, how they must be backed, and who cannot issue stablecoins. It is a much-anticipated radical reform.

What the GENIUS Act Does

The Guiding and Establishing National Innovation for US Stablecoins Act (GENIUS Act), now federal law, does something that no other statute in the United States has accomplished until now: it lays down a legal structure dedicated specifically to stablecoins used for payment.

Enacted in 2025 and titled Public Law 119-52, the GENIUS Act maps out who may issue stablecoins, under what circumstances they may be issued, and what obligations attach to those who enter this highly scrutinised market.

At its core, the law introduces an express federal framework for payment stablecoins, which it defines as any cryptocurrency or digital token pegged to the value of a fiat currency and used as a medium of exchange.

It is important to stress that this framework is focused exclusively on those stablecoins that are used in commerce as a substitute for money, not investment vehicles or crypto tokens that function in broader decentralised finance systems.

The Act speaks to the ordinary financial system and intends to integrate certain digital tokens within it, under tight supervision.

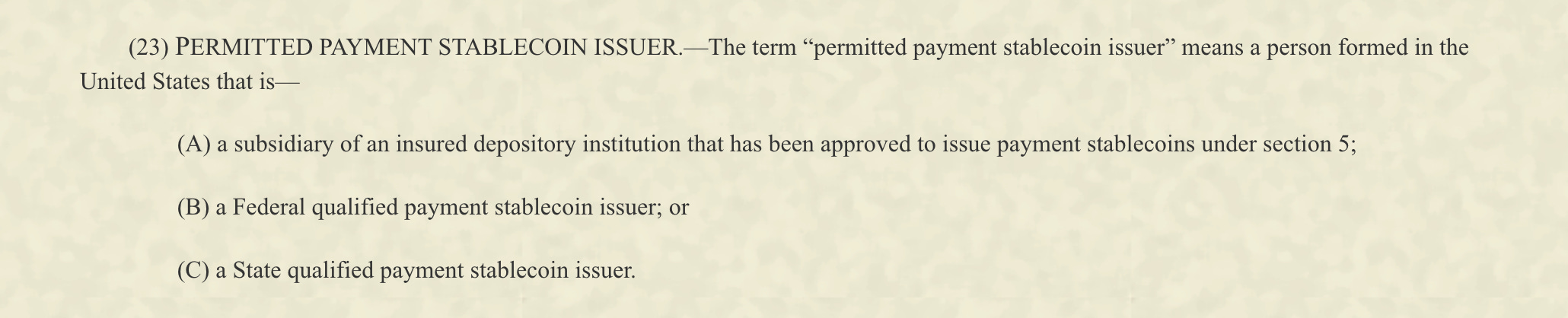

The GENIUS Act designates three categories of lawful issuers:

(1) depository institutions,

(2) non-depository trust institutions approved under federal charter by the Office of the Comptroller of the Currency, and

(3) other entities specifically authorised by state regimes that meet federal baseline standards.

Any person or organisation outside these approved categories who attempts to issue a payment stablecoin may now be prosecuted.

The legislation goes even further by explicitly excluding large technology companies and foreign-controlled entities from becoming issuers.

This marks a clear and cautious line, one that lawmakers believe is necessary to preserve financial stability and national security.

What is significant is the statutory clarity. The GENIUS Act creates rules that have immediate and serious effect.

Issuers must maintain reserves equal to the value of stablecoins in circulation, held in specific types of low-risk, highly liquid assets like US dollars, Treasury bills, and overnight repurchase agreements.

The law requires issuers to disclose how redemption works and to establish clear procedures that enable stablecoin holders to recover the face value of their digital tokens without delay. Redemption must be available at par and on demand.

The GENIUS Act mandates regular audits, risk management protocols, anti-money laundering controls, and cybersecurity standards.

All this must be reported to either the Office of the Comptroller of the Currency or a designated state regulator, with reporting obligations at least quarterly.

Failure to comply carries significant civil penalties, with the possibility of criminal enforcement in cases involving fraud or knowing misconduct.

The GENIUS Act does not express a preference for blockchain over traditional databases.

It does not define the future of digital finance in sweeping terms.

It simply carves out a space for one category of digital assets to operate lawfully inside the bounds of United States financial legal system.

Requirements for Issuers

In the finely drawn language of the GENIUS Act, being permitted to issue a payment stablecoin in the United States is not a license for experimentation but a regulatory status earned through compliance, transparency, and accountability.

The Act builds its framework on the presumption that money-like instruments require stability and reliability, and those qualities must come from law, not from market trust alone.

Every issuer must ensure that each payment stablecoin issued is backed by high-quality liquid assets held in a segregated reserve.

The Act specifies these reserves must be comprised only of certain instruments: US coins and currency, demand deposits at insured depository institutions, balances held at a Federal Reserve Bank, Treasury bills with a maturity of 90 days or less, and fully collateralised overnight repurchase agreements.

These are legislative requirements.

The legislation takes the concept of “fully reserved” literally and legally.

Section 3(b)(3)(C) of the Act makes clear that the value of reserves must equal the value of all outstanding stablecoins at all times.

There is no allowance for partial backing or investment in risky financial products.

This is cash equivalence.

Issuers must also publish, in a clear and accessible manner, the terms under which stablecoins may be redeemed by holders.

Redemption must be available at par, in legal tender, and on demand. No fees, no waiting periods, and no ambiguities.

The Act states that these disclosures must be made available on publicly accessible websites and through mobile applications. It also requires these terms to be regularly updated, with any change requiring advance public notice.

The GENIUS Act establishes further obligations in the area of risk governance.

Issuers must appoint a compliance officer, adopt written risk management procedures, and implement internal control systems that address cybersecurity, operational continuity, and counterparty exposures.

Section 3(b)(3)(F) details the need for routine internal audits, incident response plans, and controls tailored to the size and complexity of the issuer’s operations.

One particularly noteworthy element is the requirement for independent audits of reserve assets.

These audits must be conducted at least monthly by certified public accountants and submitted to the relevant federal or state regulator, depending on the issuer’s licensing status.

Issuers are also subject to anti-money laundering rules, must comply with know-your-customer obligations, and are expected to report suspicious activity under existing federal law.

The GENIUS Act brings stablecoin issuance into the fold of existing financial regulation, applying long-standing duties in a new technological context.

Impact on Foreign and Tech Firms

The GENIUS Act does more than define the conditions under which stablecoins may be issued in the United States. It also draws a deliberate boundary around who may access this space.

Foreign-controlled entities and large technology firms are, under the plain terms of this legislation, placed in a restricted category.

The law identifies their potential influence, commercial reach, and data infrastructure as reasons for caution, and that caution is written into law.

Section 3(b)(2) of the Act provides a clear exclusion.

Any company that is predominantly engaged in offering digital products or services and has more than two billion dollars in annual revenue, or more than five hundred million users worldwide, is barred from issuing payment stablecoins in the United States.

The exclusion applies to some of the largest technology platforms on the planet.

The restriction is not based on technological capability, but rather on concerns about concentration of financial power and the systemic risks that may follow.

Foreign entities are also singled out. An issuer that is directly or indirectly controlled by a foreign government, foreign political party, or any person domiciled outside the United States and lacking substantial business presence inside the country, is likewise disqualified.

Control is defined broadly. It includes the power to appoint board members, dictate management decisions, or exercise influence over the direction of the business.

The intention is to prevent offshore influence in what lawmakers have defined as a critical domestic financial function.

There is a further condition for all eligible entities with foreign affiliates or investors.

If an issuer is permitted to operate, and has foreign owners with a substantial interest, that ownership must be disclosed to the relevant regulator. Full transparency is the rule.

The law does not leave room for undisclosed arrangements or shadow partnerships. Ownership structures must be visible, auditable, and lawful.

The reasons behind these provisions are practical.

Payment stablecoins are expected to circulate as instruments of exchange, potentially used daily by consumers and merchants. Their issuers, therefore, must be subject to legal obligations that can be enforced by United States authorities.

This enforcement power cannot be guaranteed where foreign firms are concerned, especially those with no local incorporation or limited operational ties.

In the case of large technology firms, the concern is partly economic and partly constitutional.

These companies often hold enormous volumes of user data, control access to digital platforms, and maintain infrastructure that can bypass traditional financial institutions.

By placing them outside the permitted issuer class, the law anticipates conflicts of interest, monopolistic structures, and blurred lines between platform governance and monetary instruments.

What emerges is a legislative choice. The United States has decided to permit stablecoins under federal law, but only within a carefully regulated domestic system.

The GENIUS Act makes it clear that permission is contingent not only on compliance with technical standards, but also on the nature and identity of the issuer.

That wraps up our look at the GENIUS Act and its approach to stablecoins in the United States. We welcome your reflections, questions, or critiques. Feel free to comment on this newsletter.

This law does more than regulate stablecoins. It marks a clear signal from the United States that private money systems, if permitted at all, must serve public values and legal standards. Issuers now stand on a narrower, but more predictable, path. It is no longer a regulatory grey zone.