How Facebook Tried to Outsmart the IRS and Failed (Facebook, Inc. v. Commissioner of Internal Revenue)

Newsletter Issue 46 (Case Report): Facebook U.S. tried to outsmart the IRS with a $6.5B tax shuffle but the court called its bluff.

Facebook tried to migrate its valuable tech to Ireland. The IRS saw a billion-dollar money enterprise in Ireland and took them to court. What followed in a contested case decided in May 2025 was how to price the digital engine behind one of the world’s biggest social media companies. This case unpacks how Big Tech handles taxes, what regulators are doing about it, and why it all matters more than ever in the post-Meta world.

⚖️ Litigants: Facebook, Inc. v. Commissioner of Internal Revenue

🏛️ Court: United States Tax Court

🗓️ Judgment Date: 22 May 2025

🗂️ Case Number: 2025 WL 1493002

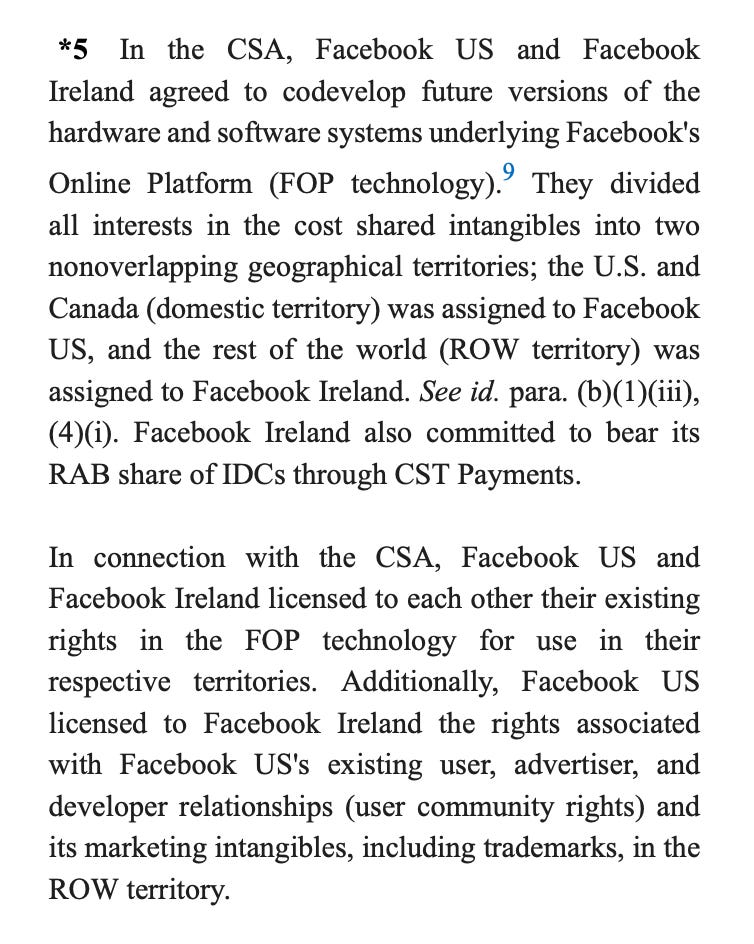

Facebook’s Irish Adventure

In 2010, Facebook was growing faster than a viral cat video. It had become the go-to social media platform for baby pictures, political rants, and suspiciously vague relationship updates.

As the company expanded globally, its attention turned not only to more users but also to smarter ways of managing its money.

Facebook attempted to circumvent tax through smaller international subsidiaries.

At the centre of this legal issue was Facebook's desire to maximise profits while limiting the reach of the United States tax authorities.

The solution, in Facebook’s view, was to share some of its valuable assets with its Irish subsidiary. By doing so, the company could tell the IRS that the real money-making entity was still based in the U.S.

To make this plan sound perfectly legitimate, Facebook used something called a “cost-sharing arrangement”, or CSA.

A CSA is essentially a deal between two related companies that agree to develop intangible assets together and share the costs.

In theory, this makes sense. If both parties are investing in the development of a technology, they should both benefit from it.

The tricky part is agreeing on how much those assets are worth.

That is where things began to get messy, ouch!

In Facebook’s case, the company handed over international rights to its core technology, its intellectual property, and the advertising platform that made it billions of dollars.

These rights were transferred to Facebook Ireland, which was a wholly owned subsidiary.

In return, Facebook Ireland would pay a share of the development costs, allowing it to use these rights outside of the United States. That was the arrangement on paper.

What followed next was a game of valuation.

Facebook informed the IRS that the package of rights it transferred to Ireland was worth about 6.5 billion dollars.

The IRS reviewed the details and responded with a figure closer to 19 billion dollars. That was not a small difference. That was the kind of difference that gets tax lawyers very excited and judges very tired.

The IRS believed Facebook undervalued its technology.

According to the IRS, Facebook Ireland was receiving access to the entire engine that powered Facebook’s advertising business around the world. This engine came with user data, ad targeting capabilities, and a growing international user base. All of that had value. And the IRS wanted its slice of the pie.

Facebook argued that in 2010, its platform was still a work in progress. It claimed the company had not yet reached its full potential and that the risk of failure was still real.

In its view, Ireland was taking a chance on a product that was not guaranteed to succeed. The IRS did not find that argument persuasive.

They looked at Facebook’s growth, its plans for global expansion, and the way the advertising platform was structured. The IRS concluded that this was not a risky startup move. This was a deliberate plan to move value offshore.

So began a long and detailed legal battle between Facebook and the Commissioner of Internal Revenue.

The simple question was: how much is Facebook’s technology really worth?

But as the court would find out, answering that question was anything but simple.

The introduction of the CSA gave Facebook a legal framework. But it also opened the door to scrutiny, and scrutiny came with spreadsheets, expert witnesses, and a some regulatory suspicion. What Facebook viewed as a savvy business decision, the IRS viewed as an overly convenient tax dodge.

Valuing the Facebook Platform

In this corner stood Facebook, armed with valuation reports, clever accountants, and a belief that what it handed over to its Irish subsidiary was worth only a humble 6.5 billion dollars.

In the other corner stood the IRS, unimpressed and suspicious, claiming that the true value of the deal was closer to 19.2 billion dollars!

What unfolded next was less of a negotiation and more of an academic brawl between economists with competing models, forecasts, and lots of graphs.

The central issue was this: what exactly did Facebook give to Ireland?

The company transferred the rights to its international platform.

This included the powerful advertising system that turned attention into revenue, the back-end architecture that made everything run smoothly, and the juicy data-driven insight into millions of users worldwide.

Facebook Ireland was suddenly responsible for all non-US markets, armed with the same tools that made the parent company rich.

Facebook argued that although this might sound valuable, it was not yet the golden goose. It was more like a “promising” goose egg.

The international business, they said, still needed to be incubated, nurtured, and possibly rescued if things went sideways.

The IRS saw it very differently.

According to the U.S. government, Facebook had essentially handed over a fully functioning money-generating enterprise with global scalability. The IRS was not impressed with Facebook’s modesty.

This dispute came down to two valuation methods.

Facebook’s experts chose the cost method. This approach looked at how much it would take to build the same technology from scratch.

Facebook U.S. answer: 6.5 billion dollars.

That number included some software development, branding, and a polite estimate of potential future costs. It was tidy and conservative. The IRS did not agree.

The IRS used the income method. This approach asked how much money the Irish business was expected to generate over time. Then it looked at how much that future income was worth in present-day terms.

This number was much higher. By the IRS’s math, Facebook Ireland had walked away with something that would help rake in over 180 billion dollars over two decades.

They applied discount rates, considered growth projections, and landed on a valuation of 19.2 billion dollars. The IRS was not aiming low.

Once the value assessment models were on the table, things turned technical very quickly. Facebook’s side brought in experts who explained that the company was in an early stage of international development.

They believed the risks were high, the future was uncertain, and the Irish subsidiary had a long way to go before it could turn serious profit.

The IRS witnesses countered this by pointing out that Facebook was already a dominant player.

They argued that the company knew exactly what it was doing and that the advertising platform was ready to grow without much extra effort.

They also suggested that Facebook’s own internal forecasts told a very different story from the cautious tale its experts were trying to tell.

The court had the unenviable task of sorting through all this litigation mess. It needed to decide which method made more sense, and which experts had applied it properly.

The cost method felt too simple for such a powerful engine. The income method seemed better suited to reflect the platform’s true earning potential.

The only problem was that the IRS got a little too creative with its numbers. Its projections were ambitious. Its inputs were not always reliable. The judge pointed this out with the tone of a teacher grading a rushed homework assignment.

In the end, the hotly contested case showed how hard it is to value a digital empire.

Facebook and the IRS both came with logic, formulas, and confidence. What they produced were wildly different conclusions about the same transaction.

Behind all the math was a simple disagreement: was Facebook being realistic, or just being very, very optimistic on paper?

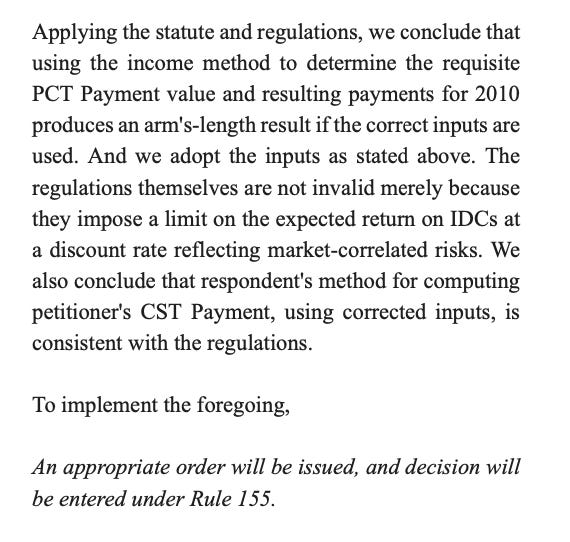

The answer, as the court would later suggest, leaned closer to the IRS valuation, but with some adjustments. The Facebook platform was valuable. The transfer had weight. And Facebook Ireland had received a lot more than Facebook U.S. had suggested.

The Legal Questions at Play

Every great tax saga must eventually come face to face with the law itself. For Facebook, that meant entering the realm of Section 482 of the Internal Revenue Code.

This section gives the IRS a powerful remedy. It allows the agency to adjust the income between related businesses so that everything reflects the way unrelated parties would deal with one another. The goal is fairness.

The IRS does not enjoy being left out of global tech profits.

Facebook argued that it had played by the rules. The IRS replied that Facebook had played the rules like a fiddle.

The courtroom soon filled with legal deliberations, regulatory disputes, and more paperwork than a small public library.

One key legal issue was how to define a “platform contribution.” This was the difference between Facebook transferring ordinary assets or giving away something essential to its business.

According to the IRS, the Facebook platform was not a side project. It was the foundation of Facebook’s entire business model. The IRS wanted it to count as a “platform contribution” under the cost-sharing regulations.

Facebook pushed back. The company claimed the international subsidiary would have to develop its own success. It argued that only certain types of intangible assets had been transferred.

The rest, including the powerful user base and the advertising algorithms, would be built further by Facebook Ireland with its own effort.

This sounded very responsible. It also sounded like something a parent says when giving their young teenager the keys to a sports car and saying, please drive slowly.

The IRS was not convinced. The agency had regulations in place that required related parties to share the costs of valuable assets and income if they had access to something important.

The IRS believed the platform was important. Facebook claimed the platform was not something that should be valued like a finished product. It was just a set of tools.

The court was left to figure out how much value was already there and how much would need to be added later.

Then came the challenge to the regulations themselves. Facebook argued that the IRS rules were invalid. This was bold.

It was one thing to say the IRS was wrong. It was another to say the IRS had no authority in the first place.

Facebook claimed the income method approved by the IRS was outside the scope of the statute! In fact, they said the IRS made up a method that Congress never allowed.

The court listened carefully. Then it disagreed.

The judge found that the IRS had authority to issue the regulations. The method the IRS used, while not perfect, was legally sound.

The court acknowledged that the IRS was allowed to create rules that helped capture economic reality. Facebook’s challenge did not get far. The judge dismissed the claim with a tone that sounded polite but very final.

Another legal question involved how to interpret risk.

Facebook suggested that since the foreign entity took on commercial risk, it deserved a fair share of future profits.

The IRS said the risk was minimal. Most of the work had already been done by Facebook in the United States.

The overseas entity was stepping into a very comfortable situation. The court agreed with the IRS on this point.

It said Facebook had not shown that the foreign entity was taking on anything close to the kind of risk that would justify a low buy-in price.

In the end, the law did not bend in Facebook’s favour.

Section 482 gave the IRS the power to adjust transactions if it looked like profits were being shifted unfairly.

The IRS had used this power confidently.

Facebook’s attempts to downplay the platform’s value, challenge the rules, and promote its own economic interpretation were noted but not accepted.

The legal questions were many. The answers were clear enough for the judge. The Facebook platform had value. The IRS had authority. And Facebook would be paying tax more than it hoped.

How Does This Outcome Impact The Digital Economy?

The Facebook tax case may have looked like a fight between two accountants with different calculators. It was more than that.

It showed how governments are trying to catch up with global tech companies that have become experts at moving money across borders faster than a meme spreads on the internet.

The key lesson is simple. Regulators are watching. When a business sends valuable rights overseas and says they are not worth much, tax authorities can take a second look.

Facebook tried to transfer the rights to its technology at a friendly price. The IRS showed up with a different opinion and a much larger number.

The court sided with the IRS, not because it liked their math, but because it found their approach closer to reality.

This ruling sends a message. Digital companies must explain clearly how they value their intangible assets. They need to back up their numbers with more than optimism.

Platforms, algorithms, user data, and advertising systems are not invisible.

Just because they cannot be touched does not mean they are not valuable.

The court treated the Facebook platform as a business asset with serious economic weight. So will other tax authorities.

The case also shows that transfer pricing for intellectual property is changing. In the past, companies might have looked at costs. They would ask how much it took to build the technology.

Now, regulators want to look at future income. They want to know how much the asset will earn. The IRS used the income method, which focuses on expected profits.

The court accepted this approach.

That puts digital businesses on notice. If they are creating tools that generate long-term revenue, the tax value must reflect that.

In the digital economy, ideas move fast. So do licenses, rights, and strategies.

Governments are trying to make sure the tax follows the value.

Companies that rely heavily on intangibles must prepare for that. They must be ready to show how value is created, where it is created, and who controls the key assets.

The court spent many pages reviewing the risks taken by Facebook’s foreign entities. The final view was that most of the valuable work had already been done in the United States.

That supported the tax case outcome.

Now that Facebook has rebranded as Meta, there are even more questions. The business model has expanded. It includes virtual reality, digital assets, and more user data than ever. That means more complicated tax puzzles.

If Meta builds a virtual world in California and licenses it in Ireland, the IRS will likely take a closer look than before.

The Facebook case made it clear that brand, platform, and user network have value. The Meta version of those assets will also have value, and probably an audit.

Digital companies can no longer assume that offshore deals will go unnoticed. Regulators have better tools, more data, and more confidence.

Courts are willing to review the full economic picture.

If a company says that its overseas branch is taking on all the risk and earning all the reward, there needs to be solid evidence.

The lesson is not just for Facebook. It applies to every tech company with a global footprint and a digital product. From e-commerce to streaming to artificial intelligence, the pressure to explain where the profits belong is growing.

The IRS may not have changed the rules, but it has shown it knows how to use them.

Tax is no longer just a filing season event. It is part of the digital economy's structure. The Facebook case made that very clear. Regulators are keeping receipts.

Consider subscribing to the Tech Law Standard. A paid subscription gets you:

✅ Exclusive updates and commentaries on tech law (AI regulation, data and privacy law, digital assets governance, and cyber law).

✅ Unrestricted access to our entire archive of articles with in-depth analysis of tech law developments across the globe.

✅ Read the latest legal reforms and upcoming regulations about tech law, and how they might impact you in ways you might not have imagined.

✅ Post comments on every publication and join the discussion.

I am amazed that they even tried to hustle the IRS.